MANAGING CASH FLOW DURING TIMES OF CRISIS:

PPT Presentation

Presented by: Jill Swinger & Richard Kannan

Finance & Accounting Services

Fractional Finance & Accounting Roles

Financial Consulting & Advisory Services

MANAGING CASH FLOW DURING TIMES OF CRISIS:

Presented by: Jill Swinger & Richard Kannan

Author: Mike Kelly

All businesses, regardless of size and industry, have one thing in common — the need for accurate financial reporting. However, a one-size-fits-all approach to keeping your books will not work. In particular, certain businesses need to be very proficient with Job Cost Accounting as they accumulate costs of materials, labor and overhead. These types of companies include manufacturers as well as real estate and related industries like developers, architects, and contractors.

Author: Stephanie Ford

Good news/bad news: Your business is expanding and achieving projected growth. The rush of growth is exciting, but it comes with a new challenge – access to capital to maintain momentum. In any credit market, financing can be tricky to obtain. You might already know this first hand — have you applied for a commercial loan and been rejected? Feeling anxious and unsure how to move forward? Here are steps to best prepare for your next meeting with a commercial banker.

Contributor: Richard Kannan, Warren Whitney Finance & Accounting Director

The larger the company, the bigger the risk of fraud, right? Well, not necessarily. On a relative basis, smaller organizations may be at greater risk. The average fraud loss for companies with less than 100 Employees is $200,000, versus larger businesses where the average fraud loss is $104,0001. Fraud losses occur when there are NOT proper controls put in place. When small to medium-sized businesses have a leaner accounting team or one person with too much authority, they become vulnerable. The fact is that inadequate controls create opportunities for fraudulent activities.

Contributor: Gene Gregory, Warren Whitney Finance & Accounting Director

Financial Management for the Non-Financial Leader

Whether you have just bought the company or have risen through the ranks, as the CEO, President, or Executive Director, you are responsible for overseeing operations, ensuring financial sustainability, and managing the organization.

If your career path has been in operations, business development or fundraising, you may feel your financial acumen is insufficient. With this lack of experience, you question how can you be confident in your role and responsibility for financial sustainability.

This is not an unusual scenario. The non-financial leader often carries this burden and can feel inadequately trained. If this is what you face, below are recommendations to follow for your organization’s financial health.

Spend some time to make sure you understand how financial transactions flow through your organization. Look for any concentration of duties or conflicts of interest that create risk. Make sure there are clear lines of authority for all financial affairs; consider both the physical and virtual security of the organization’s assets. Remember assets may be “virtual”.

KEY POINT

“Cash is King”! Embezzlement of cash is the most frequent means of misappropriation of an organization’s assets. A simple monthly review of the bank statement might identify issues and, at a minimum, puts your staff on notice that you are paying attention to the details.

Financial reports summarize your organization’s financial activities and position. Your accounting department should produce consistent and accurate financial statements. At a minimum, receive and review:

If your organization has significant accounts receivable, large capital expenses (building, equipment, etc.), or debt service requirements, the cash flow statement may tell a different story from the income statement.

Reviewing monthly and YTD income and cash flow statements will explain how the organization is progressing (or regressing). Comparative statements showing current results and positions compared to past results and positions will identify trends. Comparison to budgeted activities (see #3 below) will show how closely you are following your plan. Ideally, your staff and system(s) can report activity at the “business unit” level that is important to your organization (i.e., division, location, department, program).

Make sure your reports are relevant to your needs. External reporting likely requires financial statements prepared in accordance with the Generally Accepted Accounting Principles (GAAP); however, you may need a different view or format to make good business decisions.

Budgets are essential to good financial management because they project future revenue and spending. Your budget should be your roadmap to operations. Even if your operational managers lack budgeting experience, have them participate in the process.

Without a budget, your organization will “fly blind.” The budget outlines your operational plan in terms of revenues and expenses. How do your operations generate revenue? What is the expense structure of your organization? Asking yourself these questions and reviewing the company’s past expenditures will help guide the process (Note- Units of sales or services usually have predictable revenue values).

As mentioned above, reporting financial results versus the budget shows how you are doing against your planned operation. This comparison may indicate a need for greater skill in planning and budgeting or for a change in operations.

KEY POINT

Learn from the advisors who support your organization.

Warren Whitney

Many of our clients have found that our accounting and finance professional offer an efficient and effective solution to financial management. Our professionals work on an ongoing, part-time, fractional basis to provide a cost-effective way to supplement your finance function and build for the future. To learn more about financial management, please contact Gene Gregory at 804.977.6693 or ggregory@warrenwhitney.com

Ready or not for your year-end? – And why do we ask in January?

Start at the beginning to be ready for the end.

Do you take your fiscal year-end preparation in stride, or do you dread it? Whether your year end is December 31st, June 30th, or any other date, most likely you need to make sure your financial statements are ready for tax returns and, possibly, for auditors, bankers, and/or investors. The best way to take it all in stride is to ensure you take the proper steps monthly and quarterly for minimal work at the end of your fiscal year.

CELEBRATING WARREN WHITNEY’S 25-YEAR RELATIONSHIP WITH GOODWILL

Warren Whitney is proud of the over 25-year relationship we have enjoyed with Goodwill of Central and Coastal Virginia. While our relationship began with a series of various projects, it has deepened through the long-standing Fractional CFO role. Over the years, we have become an integral partner in Goodwill’s mission to “change lives by helping people help themselves through the power of work”. Goodwill’s workforce development services are designed to give people the life skills and job training they need in order to secure and maintain employment. As one of the first social enterprises in the U.S., much of Goodwill’s revenue is generated by people donating items such as: clothes, housewares, toys, electronics, furniture … even cars! Proceeds from reselling these items – as well as from contract services and philanthropy — allow Goodwill’s mission to become a reality.

Charles Layman, President and CEO of Goodwill of Central and Coastal Virginia, recently sat down with Stephanie Ford, Director at Warren Whitney, to dive deeper into Goodwill’s achievements and explore the role Warren Whitney has played throughout its journey of growth.

WARREN WHITNEY & GOODWILL

SF: Tell us about one of the biggest challenges Goodwill has faced and how Warren Whitney helped you overcome it?

CL: One of the biggest challenges we faced was having employees keep pace with the change in growth we were experiencing. As we hired individuals, they were often good for that particular timeframe in which they were hired. However, many didn’t have the bandwidth to take us to the next level. When we brought Warren Whitney Co-founder Scott Warren on as a fractional CFO, he gave us access to expertise we otherwise could not afford, and he took us to the next level without skipping a beat.

FRACTIONAL CFO & GOODWILL

SF: How did you know that the fractional CFO model was right for Goodwill?

CL: (1) A fractional CFO brought us a higher level of business expertise, acumen, and experience that we would not have been able to afford as a full-time expense. (2) The right fractional CFO becomes an integral part of the leadership team and strategic thinking. He or she has the ability to take our organization to a higher level and at a faster pace we otherwise wouldn’t have the capacity for, and help us to think strategically and broader.

SF: Why would you recommend a Fractional CFO?

CL: (1) The main factor is the level of experience and exposure offered in the business world. (2) The affordability of being able to bring in that high level of expertise into the organization. (3) A fractional CFO can be objective, non-emotional, and have a fresh perspective.

EVOLUTION OF WARREN WHITNEY’S ROLE AT GOODWILL

SF: How has Scott’s role evolved over the years?

CL: Scott has been involved with Goodwill in a number of engagements dating back to the 1990s. When we merged with the Hampton Roads Goodwill in 2006, consulting with Scott on new systems to improve efficiencies was instrumental as we began to manage a broader territory. These strategic discussions directed the transition as we smoothly doubled the size of our territory with limited resources. Soon after, Scott joined us as a Fractional CFO. His primary focus was debt and bond management, banking relations, cash flow, forecasting, and strategic planning. Now, in addition to that, he oversees Human Resources and IT.

THE BIGGEST VALUE IN WORKING WITH SCOTT WARREN

CL: The biggest value in having Scott Warren has been his integrity and ability to relate internally and externally; internally with our leadership team and board of directors, externally with our stakeholders. The fractional nature of his work also allows Scott to stay very involved in the community and keep his finger on the pulse of changes and opportunities that can benefit Goodwill.

ChamberRVA’s IMPACT AWARD

SF: We want to congratulate you on becoming a finalist in the “large organization” category for the 2018 ChamberRVA IMPACT AWARD. What makes Goodwill a good candidate?

CL: Goodwill gets people to work who have not been working. It is giving them the ability to become contributing citizens. We are supporting them to break barriers and move up the career ladder. Last year, over 2,000 people were placed in employment with Goodwill of Central and Coastal Virginia. When it comes to impact, we look at earnings of those people as compared to their dependence on subsidies. It builds the economy, their self-confidence, and self-esteem.

Contributor: Greg Herceg

Organizations can only be as good as their leaders; even with top talent and sufficient resources, a lack of proper management and guidance can mean the difference between failure and reaching your full potential. Fortunately, regardless of the size, revenue, or industry of the business, some leadership skills are always applicable. This newsletters outlines five important lessons in leadership that were learned from the trenches.

Contributor: Stephanie Ford

Imagine this…. Your company is growing… you need capital to continue to expand… however, you’ve been turned down by three banks in a row. Yikes! Has this ever happened to you?

In my 12 years of experience as a commercial banker, the better prepared a business owner was for the request, the more likely they would receive financing. Owners that came to me with a binder chocked full of financial statements, detailed reports, and maybe even a strategic business plan were impressive. Entrepreneurs that provided few concrete materials and simply shared a stream of consciousness of their ideas gave me little to work with.

How to position yourself to get funding for your business is critical in today’s tight credit markets. Preparing a request for financing should be taken seriously, and good preparation will yield better results. Here is a framework for thinking about your approach.

1. Think hard about why you need to borrow. Specifically identify the purpose and develop a business case for the need to borrow and repayment. The best way to do this is to prepare monthly cash flow projections of sources and uses of cash. This prediction of needs and surplus will help to identify how much you need to borrow and how quickly your business can repay the loan. The purpose of your borrowing need will also help to determine what type of loan is best for your company, such as a revolving line of credit for working capital needs or a term loan for permanent improvements to real estate or equipment purchases.

2. The more complete a package of information you can provide to the bank, the better. If you have a business plan, share the entire plan with your banker. In addition to 3 years of financial statements and tax returns, also include any other key reports that you use to run your business. This may seem excessive, but even routine reports such as an accounts receivable aging and accounts payable aging aid in giving the banker insight to your customer management and diversification. Be sure to share any key metrics that are valid for your industry, such as inventory turns, job costing reports, days to market, customer returns, utilization rates, etc. Providing organizational charts and competitive industry details is also valuable.

3. Just as important as preparing your loan request package, give serious evaluation to the bank and banker you want to work with. In today’s market, financial institutions vary widely. Consider what is important to you: branch convenience, technology and services, commercial focus and approval process, legal lending limit, ability for the bank to grow with you over time, etc. Think about whether these needs are best met by working with a large national institution, a strong regional player, or a small community bank. Once you have a sense of the type of institution that would best fit your business, research to determine the best contact at that bank for you. Most commercial banks have several bankers in one department with a manager above them. Finding the right person and personality for you to build a long-lasting relationship with can make all the difference in the growth of your business over time, particularly through the tough years.

The classic 5 C’s of Credit have been an excellent guide for many over the years on the borrowing process. If you can imagine yourself in the shoes of the banker, thinking through their concerns, it will help you prepare your request and business case.

Character

During the entire request process, the banker is also evaluating your character to try to determine if you would be a trustworthy borrower. Be sure to have your personal finances in order as well. Complete a detailed personal financial statement (any bank can provide you their form), know your credit score, and clear up any incorrect items with the credit bureaus. Provide background about your relevant experience and track record of profitability and repayment ability. This can also include any prior company experiences. Most of all, be forthcoming with both the good and any downside to your experience. Bankers never like surprises.

Capacity

You should know that the bank will be examining your financial statements and then calculating certain financial ratios. Two of the most critical ratios are leverage and debt service coverage. Leverage is measured by debt/net worth and the lower the better. While the target varies per industry, a good guideline is under 2:1. Cashflow is a measure of income/debt payments or more specifically EBITDA/(prior year’s current maturities of long term debt + interest expense). It is essential that this ratio exceeds 1.2:1.0, no matter your industry. The higher the better as you want to show the bank you have sufficient cashflow to service your debt along with a cushion for good margin.

The key takeaway: it is good if you are able to calculate these in advance so that you can anticipate how favorably your numbers will be viewed in the eyes of the bank.

Capital

This refers to your net worth or equity value in the businesswhich is determined by the value of your assets less the amount of your liabilities (how much youown minus how much you owe). The higher your net worth, clearly the better.

Note: a negative net worth is a red flag to the bank and a sign you may still be at the level of borrowing from friends and family or other non-traditional sources such as factoring receivables or venture funding.

Collateral

After the bank examines your cash flow repayment ability, they then look to collateral. Consider your business assets and personal assets you have available to offer. This may include real estate, investments, accounts receivable, inventory, equipment, and even your personal residences. How large and liquid are they in relation to the loan you are requesting? The reality is, they should be larger than your loan request as banks discount the value of most assets and only lend 40%-80% against most assets.

Conditions

If you have encountered any difficult spots in your business in the past few years, address them up front. Prepare to tell the story of your business and how you worked through the challenging times. Different banks may also have different tolerances for different industries. This may be based on the performance of the industry overall, the bank’s experience in that industry or their amount of current exposure to that industry. Ask about their preferences to find a better match and increase your success rate. Remember, no industry was untouched in the recent great recession. How you faced those challenging times will be insightful.

Seeking financing in today’s market is complex. To put your best foot forward, much preparation is needed. Seek the guidance of an advisor(s) for input into your request and positioning. Your CPA, attorney or Warren Whitney consultant can be a valuable resource in this process.

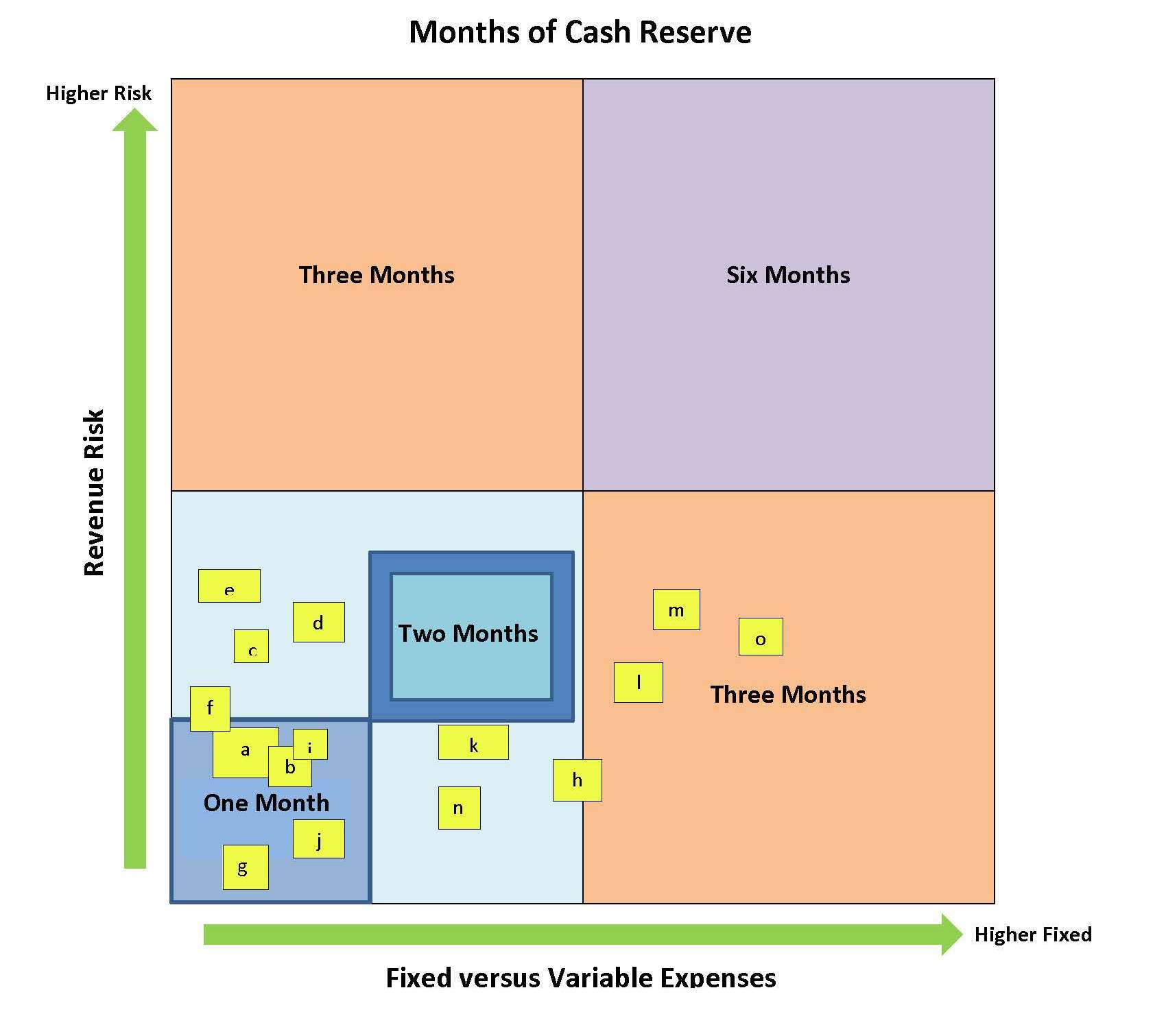

Businesses don’t always have a choice in their level of cash reserves, but having a target will help guide decisions regarding how to deploy cash. Deciding what that target should be depends on your business’s particular risk factors. There is no exact formula, but consider the two broad categories of revenue generation and fixed vs. variable expenses as a starting place and a range of three to six months of operating expenses for your cash reserve. If your risk in generating stable income and your fixed costs are both high, your cash reserve target should be closer to six months.

Try the following approach to get a sense of what type of cash reserve target you should have.

1. Start your analysis by identifying and assessing your revenue risks. These risks could include factors such as:

a. Diversity of revenues – Greater diversity equals lower risk. Consider various types of diversity, including industry, size of company, location, etc.

b. Concentration of revenue – This is the flip side of diversity of revenues. If a large percentage of your revenue comes from one source, your risk is higher.

c. Margin associated with revenue line items – Greater margins equal lower risks.

d. Control over revenue – Is your product or service necessary or optional for your customers?

e. Length of contracts – Do you have contracts? Do they span months / years? What are the terms of cancellation?

f. Market share – How likely is it that your organization will be on the “short list” as customers make their decisions.

g. Economy – How is the economy – local, national or international – based on where you draw customers?

h. Trends – Does your crystal ball show that things are getting better or worse?

i. Accounts receivable – Are you a cash business? Will you be able to collect your accounts receivable?

2. Next, identify and assess your fixed versus variable costs. More fixed costs mean higher risk because you cannot make adjustments as quickly and, therefore, a higher cash reserve target is appropriate. Consider:

j. Type of expense – Examine your fixed short-term vs. long-term expense commitments.

k. Debt service – How much do you have to pay to stay current, and what is that as a percentage of total expenses?

l. Long-term leases – Again, what are the fixed payment commitments?

m. Staff – Can you cut staff if you lose contracts? How fast are you willing to cut staff if there’s a downturn?

n. Corporate overhead – What other overhead costs are essentially fixed?

o. Variability of expense – Examine the flexibility of expense levels for different business units.

3. Finally, plot your risk assessment on a matrix where one axis represents revenue risks and the other represents fixed cost risks. See an example below.

Example of Completed Cash Reserve Matrix

Suggesting a Reserve Equal to Two Months of Expenses

(letters indicate risk factors listed above)

This methodology should provide structure to support to your estimation of cash reserves.

Phone: 804.282.9566

Email: info@warrenwhitney.com

Sign-up for our Newsletter

![]()

Warren Whitney is the sole owner of the information collected on this site. We only have access to/collect information that you voluntarily give us via email or other direct contact from you. We will not sell or rent this information to anyone.